Quick Take:

- Year to date, single-family home prices were up 20% in Alameda and 18% in Contra Costa. Similarly, condo prices rose 11% and 7%, respectively.

- Sales, new listings, and inventory all fell from June to July, likely indicating the start of the typical seasonal decline across supply and demand metrics. Inventory remains depressed but has still grown significantly in 2023, which has helped alleviate some excess demand.

- Months of Supply Inventory has declined significantly in 2023, homes are selling more quickly, and sellers are receiving a greater percentage of asking price, all of which highlight an increasingly competitive environment for buyers.

Price growth slows as fewer new listings come to market

In the East Bay, the housing market is always experiencing high demand, especially in the spring and early summer months. Increasing demand and low, but rising inventory helped drive the rapid home price appreciation that the East Bay experienced in the first half of the year. Typically, demand begins to decline in July and August, so the consistently low supply may become less of an issue. However, less of an issue doesn’t mean a non-issue. Quality new listings will certainly be sold quickly, while less desirable homes will sit on the market. This isn’t unusual, but it’s more apparent due to current mortgage rates. Potential homebuyers aren’t nearly as willing to pay a premium for a fixer upper as they were in 2020 and 2021.

In July, the median single-family home prices were up year to date across North Bay counties. As sales and new listings slow in the second half of the year, home prices typically remain stable or decline at the margins.

Inventory, sales, and new listings declined in July

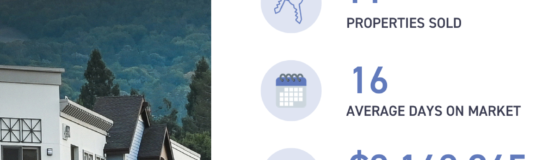

Single-family home and condo inventory, sales, and new listings rose in the first half of the year, although all remain at depressed levels. Typically, inventory peaks in July or August and declines through December or January. Single-family home and condo inventory seemed to have peaked in June, so we will likely see fewer transactions in the coming months. Currently, inventory is so low relative to demand that any amount of new listings is good for the market. However, new listings were unusually low from January through July 2023, which has directly impacted both inventory and sales. The number of home sales is, in part, a function of the number of active listings and new listings coming to market. Since January 2023, sales jumped 82% while new listings rose 52%, whereas last year, for example, sales rose 34% and new listings increased 58% by July.

As tight inventory levels continue, sellers are gaining negotiating power. In January 2023, the average seller received 95% of list price compared to 104% of list in July. Inventory will almost certainly remain historically low for the year, and the market will remain competitive in the third quarter.

Months of Supply Inventory remained under two months in July, indicating a strong sellers’ market

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The East Bay market tends to favor sellers, which is reflected in its low MSI. MSI trended lower from January to May 2023 for both single-family homes and condos. Even with the slight increase in MSI in June and July, the market still firmly favors sellers. The sharp drop in MSI occurred due to the higher proportion of sales relative to active listings and less time on the market.